As financial sins go, many Canadians would probably regard having a carryover credit card balance of $1,000 as a minor offence. After all, the average credit card debt in this country is hovering around four times as much these days, according to consumer credit reporting agency TransUnion. And that’s only a fraction of the $21,500 in non-mortgage debt that Canadians carry on average.

It turns out, though, that even a relatively “small” $1,000 credit card balance can burn a considerable hole in your pocket.

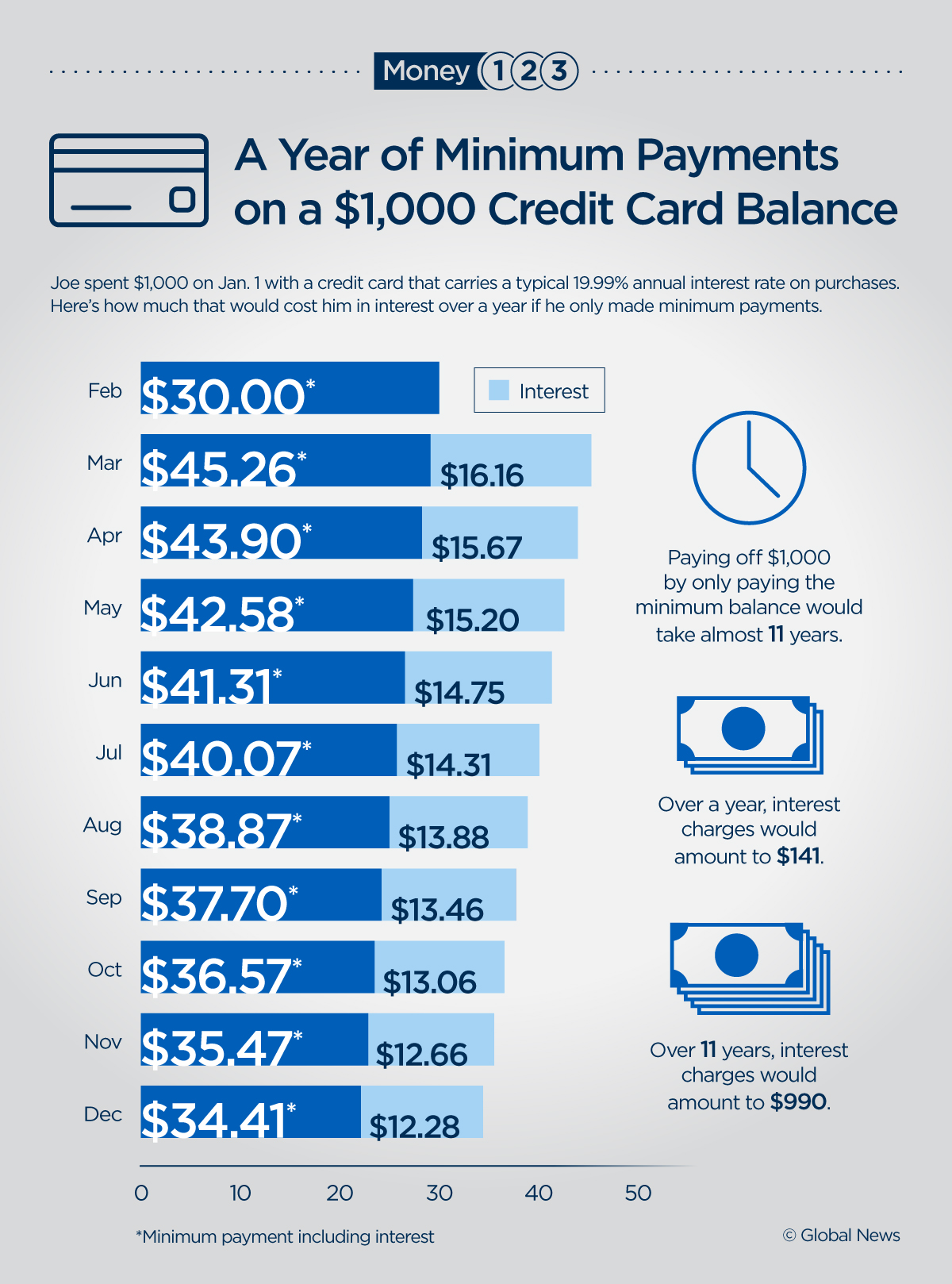

How much does $1,000 in credit card debt cost if you only make minimum payments?

Consider an imaginary scenario in which a made-up Canadian, Joe Canuck, uses his credit card to make a $1,000 purchase – let’s say a new dryer – on Jan. 1, 2018. Joe then puts that credit card on ice and proceeds to make only minimum payments on that $1,000 balance until Dec. 31.

How much will he pay in interest charges over one year? And how long would it take him to pay off that debt in full if he stuck to paying the minimum?

To help us crunch the numbers, we turned to Douglas Hoyes, licensed insolvency trustee and co-founder of Ontario-based debt consultancy Hoyes, Michalos and Associates.

READ MORE: 7 common mistakes that explain why you never have enough money

We assume that Joe has a typical “basic” credit card with an annual interest rate of 19.99 per cent on purchases. As with many credit cards, his monthly minimum payment is three per cent of the outstanding balance.

“Credit cards typically do not charge interest on purchases that appear for the first time on your credit card statement, and the payment due date is generally at least 21 days from your statement date,” according to Hoyes.

LISTEN: Erica Alini joins Tasha Kheiriddin on 640 Toronto

So let’s say Joe’s statement date is Jan. 12. His payment due date would be Feb. 2. If he paid his balance in full by then, he would get to, essentially, borrow $1,000 for over a month for zero interest, Hoyes notes.

READ MORE: 6 simple steps to get out of credit card debt

However, in our example, when Feb. 2 rolls around, Joe makes only the minimum payment of $30, or three per cent of his $1,000 balance. He pays no interest on that because it’s the first month. But interest charges will soon catch up to him.

At the beginning of March, Joe’s minimum payment has now risen to around $45, a whopping $16 of which is interest.

Here’s how that works. Joe’s outstanding balance in March has dipped to $970, or $1,000 minus the $30 he paid in February. Three per cent of that is $29, but Joe now has to pay monthly interest equal to 1/12 of his annual interest rate of 19.99 per cent, which works out to around $16. His total minimum payment is considerably higher than in February but that only reduces his outstanding balance to around $941.

READ MORE: 6 budget tips from an author who paid off almost $30K of debt in two years

If Joe keeps this up until the end of the year, he will end up paying $141 in interest and will still owe $700 of his original balance.

If Joe were to continue to make only minimum payments, it would take him almost 11 years to pay for his appliance.

And here’s the worst part: He would pay a mind-boggling $990 in interest, nearly doubling the price of the dryer.

Of course, you wouldn’t take 11 years to pay off $1,000 – but here’s the thing

Joe’s example may seem a bit of a stretch. At some point, minimum payments would drop to just a few dollars. Even the most financially stretched of us would be able to pay off the balance and save years worth of interest charges. But what if that credit card debt was the more typical $4,000 that many of us seem to carry?

The point is that “you may be paying nearly $2,000 over many years for every $1,000 you borrow on credit cards,” Hoyes said.

WATCH: Why running out of money is so easy

Compound interest is deadly when it works against you

The key takeaway here is that “compound interest is great when it works in your favour, but it’s deadly when you are paying it,” Hoyes said. Compound interest is the magic that lets your money grow by itself when you’re saving. If Joe had saved up $1,000 on Jan. 1 with a monthly interest rate of one per cent, he’d earn $10 in the first month. During the second month, he’d get another one per cent not just on $1,000 but on $1,010, and so on.

READ MORE: When saving into an RRSP instead of a TFSA could cost you dearly

When you’re carrying a credit card balance, though, you’re on the receiving end of compound interest. If you only make minimum payments, what you actually pay the credit card company can end up being far higher than the number you see on your credit card balance.

READ MORE: Here’s what taxes can do to your savings if you’re not careful

And if you get to the point where all you can afford to pay is the minimum payment, paying off that debt becomes very tough. You may need to renegotiate your debt load through a debt management program or consumer proposal to dig yourself out of the financial snowball that is compound interest when it comes to credit cards.

READ MORE: Nest-egg inequality explains why women need to save more than men

“With a consumer proposal, the average you pay is about a third of your debt, so it is very common for us to negotiate a consumer proposal where you pay $300 for every $1,000 in debt, so it’s a great way to get out of debt for an affordable cost,” said Hoyes.

WATCH: Here’s how to get out of credit card debt

Mind your credit card interest rate

The beating you can get from compound interest is greater the higher the interest is on your credit card. That’s why it’s important to be aware of the interest charges associated with each of your cards, especially if you have many, said Hoyes. When you’re repaying debt, prioritizing the balance with the higher interest is a good idea.

READ MORE: How much do you really need for retirement? We did the math

Mind your credit card utilization, too

Carrying a credit card balance doesn’t necessarily damage your credit score if you keep making minimum payments on time. But that’s not the end of the story, according to Hoyes: “Your credit score is based on a number of factors, but one of them is utilization, or what percentage of your total borrowing limit you are actually borrowing.”

Though consumer credit reporting agencies are tight-lipped about the exact formula behind credit scores, Hoyes advises keeping your utilization rate below 20 per cent to avoid a downgrade.

READ MORE: 3 things you probably didn’t know about your credit score

There are other interest rates you may be dealing with – and they’re probably going up

Credit card interest rates don’t seem to move in lockstep with other interest rates in Canada, according to Hoyes. So the fact that things like mortgage rates are climbing doesn’t mean your credit card rate will follow. Still, if your mortgage payment goes up, that will leave less money in your pocket to throw at your credit card debt.

TransUnion has predicted a rise in credit card delinquencies this year as higher rates on other loans force more Canadians to miss minimum payments.

READ MORE: Your debt in 2018: The economic trends that could hit your pocketbook

Paying even a few dollars above your minimum payment makes a huge difference

Now for the good news: Boosting your credit card payments by even a few dollars over the minimum works miracles. According to the credit card payment calculator of the Financial Consumer Agency of Canada, if Joe had bumped up his monthly repayments by just $5, for example, he would have saved nearly $380 in interest and been able to pay off his balance almost four and a half years earlier.

TO CELEBRATE THE LAUNCH OF THE MONEY123 NEWSLETTER WE’RE GIVING OUT $500:

Disclaimer – Global News provides the information contained in this series for informational purposes only. It is not to be used or construed or relied upon as financial, legal, tax, accounting or other professional advice or recommendations regarding the suitability, profitability or potential value of any particular investment, product, service or course of action. The information provided does not replace consultations with professional advisors and it is recommended that you seek appropriate independent advice from qualified professional advisors before making any financial or other decisions. Global News shall not be responsible or liable in any way for any loss or damage directly or indirectly incurred as a result of, or in connection with, the use of such information by you.

Comments